What the SVB Collapse Taught Me About Listening To Wants versus Understanding Needs

When Silicon Valley Bank collapsed over 48 hours in March 2023, I barely understood what I was reading. The headlines were everywhere, but the vocabulary was unfamiliar: held-to-maturity portfolios, unrealized losses, uninsured deposits, MRAs (Matters Requiring Attention, formal regulatory findings requiring a documented response). I filed it away as something significant that I did not yet have the framework to fully absorb.

Two years later, I started a contract at Fiserv working on a legacy banking application with roots going back three decades. The domain had its own vocabulary, its own regulatory architecture, its own way of understanding risk, and I was aware from the start that I needed to build genuine fluency before I could do the work well.

My instinct, when that happens, is to go upstream. Not only to the product documentation or the feature list, but also to the environment the product operates in. The SVB failure was sitting there, two years seasoned, thoroughly documented by regulators and researchers, and rich enough to function as a narrative scaffold for almost every fundamental concept I needed to understand. I used it as one.

What I did not expect was how completely it would also reframe the way I think about listening to stated needs.

A Bank That Outgrew Itself

SVB was in its 40th year when it failed. For nearly 38 of those years, it operated as a boutique, relationship-driven lender to the venture capital ecosystem, a specialized institution with governance structures, risk culture, and institutional reflexes suited to its size.

Then the 2020 and 2021 technology funding boom force-fed it deposits it had no organizational maturity to manage responsibly.The bank's balance sheet expanded dramatically. Its market capitalization grew to over $44 billion. It became the 16th largest bank in the United States.

The culture did not scale with the capital.

This is the foundational fact about SVB that the more technically interesting details of its failure tend to obscure. It is not primarily a story about interest rate risk, though interest rate risk was the mechanism. It is a story about an institution that had not yet become what its balance sheet said it was.

Understanding that changes how you read everything that came after.

The Depositors Worth Examining More Closely

One of the quieter details of the SVB story is how the bank's deposit base was structured, and why.

SVB's clients were largely venture capital-backed startups, companies that were burning cash rather than generating it. These depositors were skittish about lockup periods. They wanted simple deposit accounts, liquid and accessible, and they wanted them now. Most were depositing well above the FDIC insurance limit of $250,000, which meant they were technically exposed, but in practice they were not thinking about FDIC coverage. They were thinking about runway.

SVB, eager to serve and retain this client base, was accommodating. The bank offered what its clients asked for. The result was a deposit base that was both highly concentrated in a single industry sector and almost entirely uninsured. When the Federal Reserve Board later documented what had gone wrong at SVB, the reliance on uninsured deposits was identified as one of the two structural vulnerabilities that made the bank uniquely fragile.

The lesson that keeps surfacing here is an old one in research: what clients say they want is often a description of the immediate problem, not the underlying condition. SVB's depositors said they wanted liquidity. However, what they needed was a bank that understood what their request actually required on the other side of that relationship. Providing liquidity (demand deposits, freely withdrawable at any moment) to an almost entirely uninsured, sector-concentrated deposit base has direct structural consequences for how a balance sheet must be managed. A bank holding that kind of liability needs short-term, easily liquidated assets it can draw down in sequence to meet withdrawal pressure. Long-dated Treasuries are not that. SVB accepted the stated want without examining that condition.

The Exposure in Plain Sight

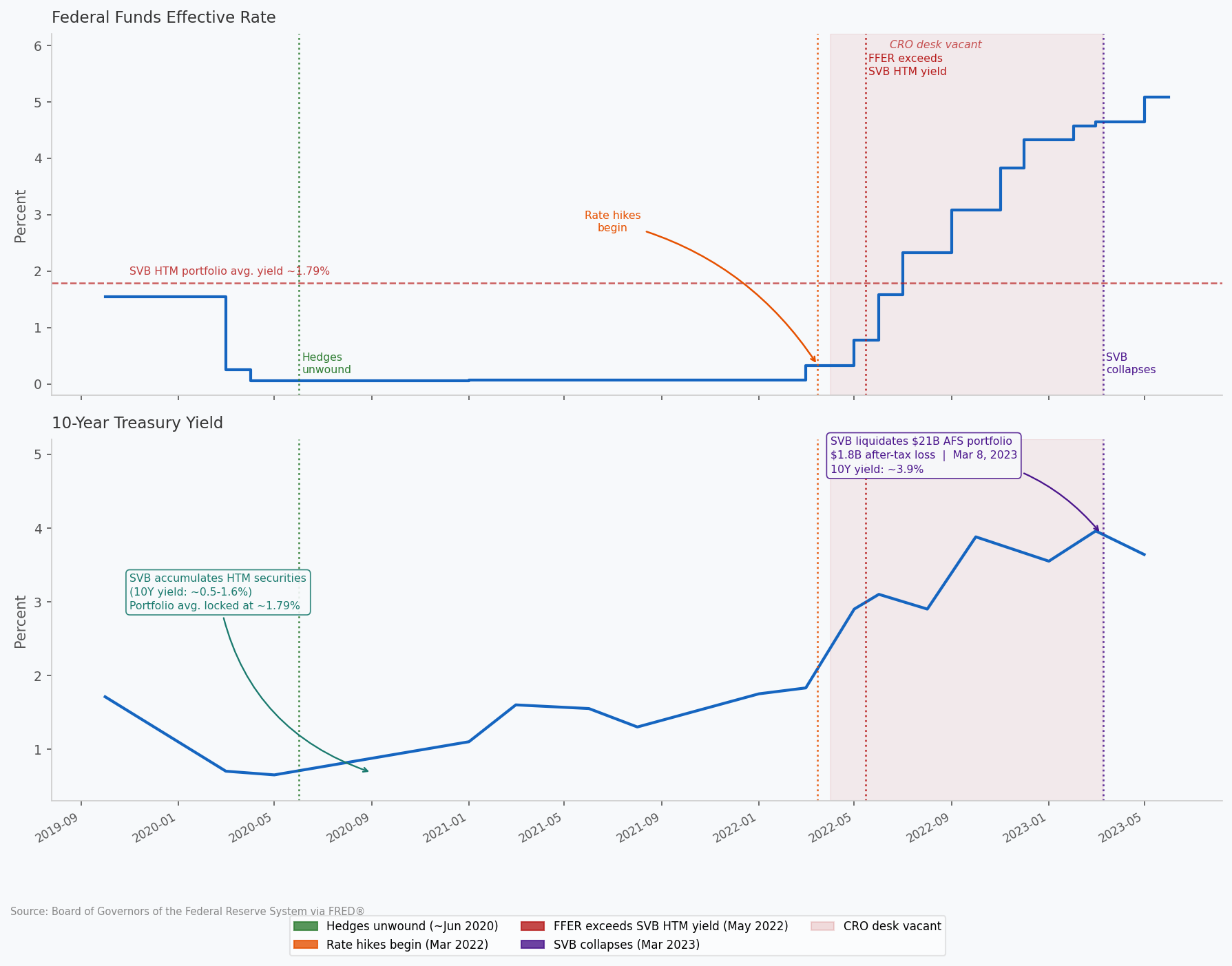

In 2020, flush with new deposits and operating in a near-zero interest rate environment, SVB invested heavily in longer-dated Treasury securities and agency mortgage-backed securities. The 10-year Treasury yield was sitting between 0.5 and 1.6% during the accumulation window, and SVB locked in a portfolio average yield of approximately 1.79%. The result was a textbook duration mismatch: long-dated assets funded by short-duration liabilities, with no hedge in place to absorb the gap if rates moved.

At the same time, the bank unwound its interest rate hedges. The rationale was defensible if you froze your assumptions at that moment: rates were near zero, hedges have a cost, and there was no near-term signal of meaningful rate increases.

The problem is that "when everything looks fine" is exactly when insurance is cheapest to maintain.

The two charts below show what happened next more directly than any narrative can.

SVB's securities portfolio was classified in two buckets with meaningfully different accounting treatment. Held-to-maturity (HTM) securities are carried at book value; unrealized losses don't appear on the income statement as long as the bank intends to hold them to maturity. Available-for-sale (AFS) securities are marked to market, meaning losses are recognized as they accumulate.

The Federal Reserve began raising rates in March 2022. By May, the Federal Funds Effective Rate had crossed SVB's HTM portfolio yield of 1.79%. From that point, every hike deepened the unrealized loss position. For most of the rate-hike cycle, SVB's mounting losses lived in the HTM portfolio: present on the balance sheet, but not forcing a crisis. When the bank needed liquidity and sold $21 billion from its AFS portfolio, it converted paper losses into realized ones that had to be publicly disclosed. By the time SVB announced that AFS liquidation on March 8, 2023, the 10-year yield was approaching 4%, and the gap between what the portfolio was worth and what SVB had paid for it had become impossible to paper over. That disclosure was what started the clock.

The unrealized losses were not secret. They appeared on the balance sheet. What was missing was the organizational capacity to act on them.

The Empty CRO Chair

During the entire period from the first rate hike through thecollapse, from March 2022 to March 2023, SVB's Chief Risk Officer position sat vacant.

The Federal Reserve Bank had been issuing Matters Requiring Attention and Matters Requiring Immediate Attention to SVB during this period. These are formal supervisory findings. They are documented. They are delivered through proper channels. They require formal responses.

They went unaddressed.

This is the detail that closes off the charitable interpretations. The bank's exposure was not hidden from leadership. Regulators had seen it, named it, and issued formal findings with their own category of urgency. The CRO position sat vacant. And nothing happened.

The failure was not a failure to detect risk. It was a failure to respond to risk that had already been detected, formally documented, and officially communicated. That distinction matters enormously, because the design interventions for those two failure modes are completely different. You cannot solve a governance failure by improving your sensing instruments.

What Collapsed in 48 Hours

On March 8, 2023, SVB announced that it had sold $21 billion from its available-for-sale portfolio at an after-tax loss of $1.8 billion and was simultaneously seeking to raise $2.25 billion in new capital. The announcement was intended to bolster depositor confidence. It had the opposite effect.

A capital raise through share issuance works under a specific set of conditions. Issuing new shares dilutes existing shareholders, meaning their stake in the company shrinks. That is acceptable, even welcomed, when the raise is in service of a growth thesis: here is the market opportunity, here is the plan, the dilution you absorb now buys expansion that makes your shares worth more later. Investors will take that trade. What SVB was offering was different. There was no market to capture, no expansion narrative, no trajectory to buy into. There was a hole to cover. That is a different instrument being asked to do a job it was not designed for, and it was being offered to exactly the audience most likely to recognize the difference.

The logic was sound in theory: proactively raising capital is what a well-managed bank does when it identifies a gap. It signals that leadership sees the problem and is moving to address it. But that framing requires a depositor base that reads the announcement the way an institutional investor would, as evidence of control rather than evidence of crisis.

The disclosure was not a communications blunder in any simple sense. SVB had SEC obligations once the loss was realized, and silence was not available to them. They worked with Goldman Sachs to line up the capital raise in advance and couldn't get it fully subscribed, meaning they couldn't find enough investors willing to buy all the new shares they needed to sell. This may have had something to do with the fact that SVB had, in the same breath, just disclosed $1.8 billion in realized losses on a portfolio that had been quietly deteriorating for months, while offering no credible path to address the structural conditions that produced those losses, and no growth strategy that might have made the dilution worth absorbing.

What made any announcement self-defeating was the structure of the depositor base itself. That evening, SVB's CEO Greg Becker held a call with major venture capital clients urging calm. At a bank whose depositors are millions of ordinary people who don't know each other, direct outreach from leadership can slow a panic. In SVB's case, it traveled at venture speed through a network where the same investors held relationships across hundreds of portfolio companies simultaneously. The reassurance confirmed there was something to be calm about. Peter Thiel's Founders Fund began advising portfolio companies to withdraw deposits that same evening.

The speed of what followed was itself a product of the depositor structure SVB had built to accommodate what its clients said they wanted: full withdrawal on demand. On March 9th, $42 billion in deposits left the bank. On March 10th, SVB informed regulators it could not meet its obligations and was declared insolvent that morning.

The Federal Reserve stood up the Bank Term Funding Program the following Monday to contain contagion. It worked. But the bank was gone.

Why Any of This Belongs in a UX Research Portfolio

The connection I am making is not that banking collapses and software usability studies are equivalent problems. They are not.

The connection is methodological. It is about what happens when you accept the stated need without examining the conditions that produced it.

SVB's depositors stated a want: liquidity, simplicity, no lockups. SVB accommodated it. SVB's loan book, meaning the record of who they were willing to lend money to, tells a quieter story. Most of these same depositors, the VC-backed startups burning through successive funding rounds, appear nowhere in it. In part, this is simply because companies flush with cash don't need loans. But SVB's credit culture also knew what it was looking at: pre-revenue entities with no collateral, no demonstrated path to profitability, and no assets of appreciable value beyond the next funding round. You don't build a 38-year institution without learning to recognize a credit risk when it walks in the door.

What that means is that the structural fragility wasn't a failure of diagnosis. SVB understood its depositors well enough to decline lending to most of them. It was a failure to let what the credit side understood speak to what the deposit side was building, to allow the same judgment that protected the loan book to inform the institution's exposure on the liability side. The risk wasn't invisible. It was compartmentalized.

In the research projects I run in enterprise software, I encounter a version of this regularly. A product team presents a request framed as a user need. A stakeholder describes what clients are asking for. The presenting request is real. What it describes, though, is often a symptom of a condition that is not yet visible in the request itself.

The complication is that neither party is usually being careless. Product teams surface what customers tell them, and customers often experience their wants as needs. The framing is sincere, not strategic. The researcher's job isn't to correct the stated request but to hold it lightly enough to ask what condition produced it.

The On-Site Leasing project at RealPage (linked to my portfolio Work section) began as a request for sales testimonials. The underlying condition, confirmed through existing data before a single session was scheduled, was that there were no net-new clients. The testimonials did not exist. Accepting the request at face value would have produced six weeks of recruiting effort aimed at a participant population that was not there.

The banking domain learning I did around the SVB collapse did not directly produce a research deliverable. What it produced was a mental model for how environments shape the systems operating within them, and how understanding that environment changes what questions are worth asking. When I arrived at Fiserv, I had already spent months reading regulatory source material, Federal Reserve examination frameworks, and the documented history of a bank failure that illustrated every major concept in the domain simultaneously.

That preparation made the research better. Not because I knew more than the participants, but because I could hear what they were actually describing rather than just what they were saying.

That is, in the end, what domain knowledge is for.

For readers interested in the Federal Reserve's own account of the 2023 banking turmoil and the design of the Bank Term Funding Program established after SVB's collapse, the Federal Reserve Board's Finance and Economics Discussion Series paper is available here.

To see both sides of this in primary sources from SVB's own perspective, two other documents are worth comparing. The Q4 2022 earnings presentation, delivered to investors on January 19, 2023, describes the bank as "strong and well-positioned" with "ample liquidity" and "continued confidence" in its strategy. Seven weeks later, on February 24, SVB filed its annual 10-K with the SEC, where the same portfolio is described in careful, hedged language: whether unrealized losses would become realized depended on "a variety of factors." The bank did not survive to report Q1 2023 earnings. Both documents are publicly available.